UK Car Market Statistics: Q1 and Q2 2026

Published May 15, 2026

- Over two million used cars changed hands in Q1 2026, though a marginal -0.2% dip ended a 12-quarter growth streak.

- New car registrations reached 149,247 in April 2026, up 24.0% YoY, the strongest April since 2019.

- Electrified vehicles accounted for 53.2% of new car registrations in April 2026, the second month this year they have outnumbered ICE registrations.

- As of April 2026, the Jaecoo 7 is the UK's most popular new car of 2026, having entered the top 10 for the first time in September 2025 and never looked back; climbing to third place overall in Q1 with 17,668 registrations, despite not featuring in last year's full-year rankings at all!

- Used BEV transactions rose 32.0% YoY in Q1 2026 to a record 86,943 units, with a 4.3% market share.

This quarterly guide brings together the latest UK used and new car market data for journalists, industry professionals, and car buyers. It covers used and new car transactions, powertrain trends, best-selling models, fleet and private demand, the UK car parc, and long-term registration trends.

For a detailed breakdown of the UK's electric car market, see our EV market statistics guide.

Get a free valuation

2026 UK used car market analysis

| Period | Transactions | YoY change |

|---|---|---|

| Q1 2026 | 2,016,232 | -0.2% |

| Q1 2025 | 2,020,990 | n/a |

| Full year 2025 | 7,807,872 | +2.2% |

| Full year 2024 | 7,643,180 | n/a |

Source: SMMT

The total transactions for Q1 2026 remain above the average run rate implied by full-year 2025.

The drag was March, which fell -2.3% against the strongest comparable since 2017, when March 2025 became the first to exceed 700,000 transactions in eight years.

2025's full-year total of 7,807,872 was the third consecutive year of growth, with ten of twelve months recording positive YoY movement.

The average age of the UK vehicle parc has reached a new high of 9.7 years, up from eight years in 2019, a reminder that used car supply depends on a healthy new car market upstream.

webuyanycar's head of technical services, Richard Evans said:

“The Q1 2026 result is better read as a pause than a reversal. March was always going to be a difficult comparison after 2025's exceptional performance, and a quarterly total of over two million transactions shows the underlying market remains healthy.”

“The used sector is gradually but consistently changing its powertrain mix. Petrol dominates and will for some time, but HEV and BEV volumes are growing at a rate that reflects a genuine shift in what is coming through from the new car market into second-hand supply.”

Used car sales Q1 2026: Breakdown by powertrain

| Fuel type | Q1 2026 | YoY change | Share Q1 2026 |

|---|---|---|---|

| Petrol | 1,147,969 | -0.2% | 57.0% |

| Diesel | 629,987 | -6.7% | 31.2% |

| HEV | 128,039 | +29.6% | 6.4% |

| BEV | 86,943 | +32.0% | 4.3% |

| PHEV | 20,021 | -14.9% | 1.0% |

| Total | 2,016,232 | -0.2% |

Source: SMMT

Key takeaways

- Petrol held a 57.0% share in Q1 2026, broadly stable YoY, continuing to anchor the used market on familiarity, affordability, and parc volume.

- Diesel fell -6.7% in Q1 2026 and -3.3% across full-year 2025, reflecting reduced supply from the new car market.

- BEVs grew +45.7% in full-year 2025 and +32.0% in Q1 2026, reaching a record 4.3% used market share.

- HEVs were the largest electrified category by volume in Q1 2026 at 128,039 transactions, up +27.6%, driven by earlier hybrid registrations now cycling into second-hand supply.

- PHEV transactions fell -8.9% in Q1 2026 to 20,021 units, comprising 1.0% of the used market.

- Combined electrified vehicles (BEV, HEV, PHEV) accounted for 11.7% of Q1 2026 used transactions, up from approximately 9.9% in full-year 2025.

Used car trends

- Superminis were the most popular used purchase in Q1 2026 at 648,229 transactions (32.2% share), followed by lower medium cars at 546,249 units (27.1%).

- DPVs recorded the strongest segment growth at +5.4% to 357,295 units in Q1 2026, while multipurpose vehicles saw the sharpest decline at -6.5% to 69,886 units.

Source: SMMT

Best-selling used cars Q1 2026 vs 2025

| Best-selling models Q1 2026 | Transactions | Best-selling models Q1 2025 | Transactions |

|---|---|---|---|

| Ford Fiesta | 76,745 | Ford Fiesta | 79,617 |

| Vauxhall Corsa | 62,201 | Vauxhall Corsa | 65,009 |

| Volkswagen Golf | 56,236 | Volkswagen Golf | 58,080 |

| Ford Focus | 54,662 | Ford Focus | 57,956 |

| Nissan Qashqai | 42,214 | Mini | 41,439 |

| Volkswagen Polo | 39,159 | BMW 3 Series | 40,810 |

| BMW 3 Series | 37,621 | Vauxhall Astra | 39,726 |

| Mini | 37,438 | Volkswagen Polo | 39,179 |

| Vauxhall Astra | 35,340 | Nissan Qashqai | 38,364 |

| BMW 1 Series | 32,363 | BMW 1 Series | 32,597 |

Source: SMMT

The top four models are identical in both periods, with the Fiesta, Corsa, Golf and Focus holding their positions. All four recorded modest YoY volume declines, consistent with the overall Q1 2026 market dipping -0.2%.

The Ford Fiesta's continued lead is notable given production ended in 2023. Its long run and historically high new car volumes mean millions remain in circulation at accessible price points.

The most notable shift is the Nissan Qashqai, rising from ninth in Q1 2025 to fifth in Q1 2026, consistent with growing DPV demand. The Mini fell from fifth to eighth over the same period.

The BMW 1 Series held tenth place in both periods. The Audi A3, which featured in the full-year 2025 top 10, does not appear in either quarterly ranking.

Superminis and hatchbacks dominate both top 10s, but the Qashqai's rise from ninth to fifth reflects the gradual shift in used market composition as SUVs establish a firmer foothold in the rankings.

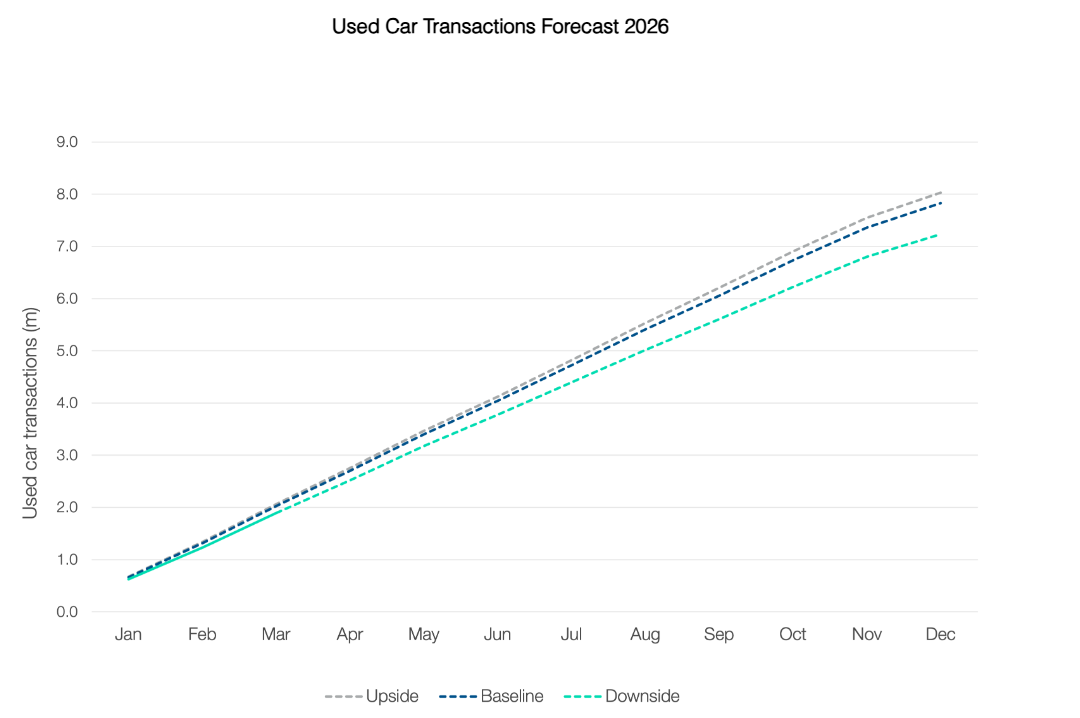

Used car market predictions for 2026

| Scenario | 2026 projected volume | YoY change vs 2025 |

|---|---|---|

| Upside | 8,026,607 | +2.8% |

| Baseline | 7,827,658 | +0.3% |

| Downside | 7,234,099 | -7.3% |

Key forecast takeaways

- Market stability expected: Cox Automotive's baseline forecast projects 7,827,658 used car transactions for full-year 2026, a marginal +0.3% increase on 2025's 7,807,872, pointing to a broadly stable market.

- Potential for modest growth: The upside scenario of 8,026,607 would be the first time annual used transactions have exceeded eight million since 2017, when 8,113,020 used cars changed hands.

- Downside risk remains: The downside scenario of 7,234,099 represents a -7.3% contraction on 2025.

Sources: Cox Automotive (Insight Quarterly Q1 2026, published April 2026); SMMT

New car market statistics: April 2026

The UK new car market rose 24.0% YoY to 149,247 registrations in April 2026. The increase partly reflects a weak April 2025 base, when buyers pulled purchases forward to March ahead of VED and ECS changes applying to BEVs for the first time. April 2026 was nonetheless the strongest April since 2019.

| Powertrain | Apr 2026 | Apr 2025 | % change | Share Apr 2026 | Share Apr 2025 |

|---|---|---|---|---|---|

| BEV | 39,084 | 24,558 | +59.1% | 26.2% | 20.4% |

| HEV | 19,711 | 16,586 | +18.8% | 13.2% | 13.8% |

| PHEV | 20,597 | 14,073 | +46.4% | 13.8% | 11.7% |

| Petrol | 63,541 | 58,733 | +8.2% | 42.6% | 48.8% |

| Diesel | 6,314 | 6,381 | -1.0% | 4.2% | 5.3% |

| Total | 149,247 | 120,331 | +24.0% |

Please note: MHEV registrations are included within petrol and diesel figures in SMMT reporting.

Source: SMMT

Powertrain trends

- Electrified vehicles (BEV, PHEV, HEV) accounted for 53.2% of April registrations, the second month this year they have outnumbered ICE registrations.

- PHEVs recorded the strongest proportional growth at +46.4%, reaching a 13.8% share, suggesting car buyers are adopting plug-in hybrid technology as a transition step.

- BEVs rose 59.1% to 39,084 units and a 26.2% April share. The rate is amplified by April's distorted base month.

- YTD, BEVs hold a 23.1% share against a ZEV Mandate target of 33% for 2026.

- Petrol volumes grew 8.2% from a low base, but market share fell from 48.8% to 42.6%.

- Diesel fell -1.0%, covering just 4.2% of the market.

Sources: SMMT

The gap between fleet and private demand

| Channel | Apr 2026 | Apr 2025 | % change | Share Apr 2026 | Share Apr 2025 |

|---|---|---|---|---|---|

| Fleet | 90,462 | 71,340 | +26.8% | 60.6% | 59.3% |

| Private | 56,116 | 46,671 | +20.2% | 37.6% | 38.8% |

| Business | 2,669 | 2,320 | +15.0% | 1.8% | 1.9% |

| Total | 149,247 | 120,331 | +24.0% |

Source: SMMT

Fleet registrations led the recovery at +26.8% to 90,462 units, accounting for 60.6% of April registrations.

Private buyers grew 20.2% to 56,116, but accounted for only 37.6% of registrations.

webuyanycar's head of technical services, Richard Evans said:

“Fleet and private demand are both growing, but for different reasons. Fleet buyers have clear financial incentives to go electric through benefit-in-kind tax structures, while private buyers are returning on the back of improved choice, the Electric Car Grant, and more competitive pricing across petrol, hybrid and electric options alike.”

New car market trends: January to April 2026

| Powertrain | YTD 2026 | YTD 2025 | % change | Share 2026 | Share 2025 |

|---|---|---|---|---|---|

| BEV | 176,698 | 144,749 | +22.1% | 23.1% | 20.7% |

| HEV | 111,083 | 102,591 | +8.3% | 14.5% | 14.6% |

| PHEV | 99,263 | 67,759 | +46.5% | 13.0% | 9.7% |

| Petrol | 340,230 | 345,520 | -1.5% | 44.5% | 49.3% |

| Diesel | 36,827 | 40,214 | -8.4% | 4.8% | 5.7% |

| Total | 764,101 | 700,833 | +9.1% |

- PHEVs recorded the strongest YTD growth at +46.5%, with market share rising 3.3 percentage points from 9.7% to 13.0%.

- Petrol and diesel combined accounted for less than half of new car registrations YTD through April 2026, at 49.3%, reflecting the ongoing shift in powertrain preference as electrified vehicles continue to gain share.

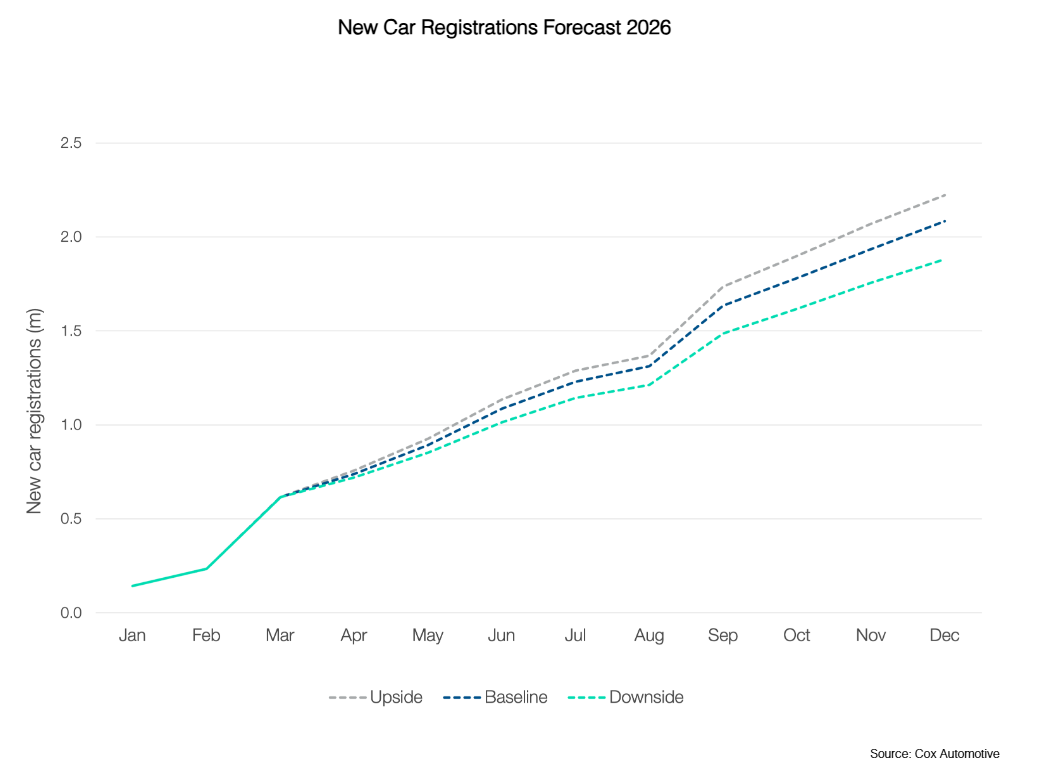

- Cox Automotive's Q1 baseline forecast projects 2,082,665 full-year registrations, a 3.1% increase on 2025, broadly in line with the SMMT's April 2026 outlook of 2.093 million.

- The downside scenario of 1,881,043 would represent a -6.9% contraction, while the upside of 2,222,587 would be the highest annual total since 2016.

Sources: SMMT, Cox Automotive

ZEV Mandate: targets and market reality

The ZEV Mandate requires 33% of each manufacturer's 2026 new car registrations to be zero-emission. The market-wide BEV share stands at 23.1% YTD through April, approximately 9.9% below that level.

The SMMT revised its full-year 2026 BEV forecast from 28.5% to 26.8% following a below-target Q1. At the revised forecast, the market would end 2026 around 6.2 percentage points below the mandate target.

Sources: GOV.UK; SMMT

Best-selling new car models YTD 2026 vs 2025

| YTD 2026 (Jan–Apr) | Registrations | YTD 2025 (Jan–Apr) | Registrations |

|---|---|---|---|

| Ford Puma | 20,339 | Ford Puma | 18,241 |

| Kia Sportage | 17,835 | Kia Sportage | 16,380 |

| Jaecoo 7 | 17,668 | Nissan Qashqai | 13,989 |

| Nissan Qashqai | 15,699 | Vauxhall Corsa | 13,852 |

| Vauxhall Corsa | 12,788 | Nissan Juke | 12,373 |

| Volkswagen Golf | 12,021 | Volkswagen Golf | 12,348 |

| Volvo XC40 | 11,360 | MG HS | 11,016 |

| MG HS | 11,293 | Volkswagen Tiguan | 10,664 |

| Mini Cooper | 10,686 | Volvo XC40 | 10,612 |

| Volkswagen Tiguan | 10,252 | Hyundai Tucson | 10,496 |

Source: SMMT

The Ford Puma leads YTD in both periods, extending its best-seller status from 2024 and 2025. Its availability in a fully electric variant, the Puma Gen-E, broadens its appeal across fleet and private channels.

The Jaecoo 7 is a significant new entry, taking third place in 2026 with 17,668 registrations against no presence in the YTD 2025 top 10. The Chery Group brand entered the UK market in 2024.

The Nissan Juke drops out of the 2026 top 10 entirely, replaced by the Jaecoo 7 and Mini Cooper. The Hyundai Tucson also drops out.

No pure BEV features in either top 10, though the BEV segment holds a 23.1% market share YTD, spread across a wide range of models at lower individual volumes.

How many cars are there in the UK?

According to DVLA vehicle licensing statistics, at the end of December 2025 there were approximately 34,485,500 licensed cars on UK roads, a marginal decrease on the 34,486,300 recorded at the end of September 2025.

UK new car sales statistics (2011–2027)

| Year | Registrations |

|---|---|

| 2027* | 2,121,000 |

| 2026* | 2,093,000 |

| 2025 | 2,020,520 |

| 2024 | 1,953,420 |

| 2023 | 1,903,054 |

| 2022 | 1,614,063 |

| 2021 | 1,647,181 |

| 2020 | 1,631,064 |

| 2019 | 2,311,140 |

| 2018 | 2,367,147 |

| 2017 | 2,540,617 |

| 2016 | 2,692,786 |

| 2015 | 2,633,503 |

| 2014 | 2,476,435 |

| 2013 | 2,264,737 |

| 2012 | 2,044,609 |

| 2011 | 1,941,253 |

*Forecast figures for 2026 and 2027 are from the SMMT's April 2026 New Car and Van Outlook and are projections, not actuals.

Car market glossary

| Term | Definition |

|---|---|

| YoY | Year-on-year |

| YTD | Year-to-date |

| Powertrain | The system responsible for generating a vehicle's power and transferring it to the road |

| Market share | Share of cars sold or registered over a specified period, not share of the overall car parc |

| BEV | Battery electric vehicle |

| PHEV | Plug-in hybrid electric vehicle |

| HEV | Hybrid electric vehicle |

| MHEV | Mild hybrid electric vehicle |

| ICE | Internal combustion engine |

| DPV | Dual purpose vehicle |

| SMMT | Society of Motor Manufacturers and Traders |

| DVLA | Driver and Vehicle Licensing Agency |

| VED | Vehicle Excise Duty |

| ECS | Expensive Car Supplement |

| ZEV | Zero emission vehicle |