What is a hire purchase?

Last updated May 21, 2021

Buying a car is a major decision and while choosing your ideal make and model is exciting, considering your finance options is crucial. If you cannot pay for the car upfront, a Hire Purchase (HP), could be an option.

Throughout this guide we have explained how a Hire Purchase works, the benefits and drawbacks and what to look out for to help you decide whether HP finance is suitable for you.

Value your car in under 30 seconds

What is Hire Purchase?

Hire Purchase (HP) is a popular choice of car finance for those who want to own a vehicle, but don’t have the funds to purchase one outright. A HP agreement is similar to taking out a personal loan to fund a car, but with a couple of key differences.

For the duration of your HP contract, you won’t own the vehicle like you would if you used a personal loan. Instead, you’ll assume ownership after you’ve made all your repayments, including the deposit, monthly payments and ‘optional purchase fee’ at the end of the contract.

The other main difference is that the debt is secured against the car, so if you can’t meet the monthly payments, the finance company could repossess the vehicle to settle the debt. This reduces the lender’s risk as the finance is secured, meaning you may be more likely to get accepted for a Hire Purchase agreement if you’ve been declined for a personal loan.

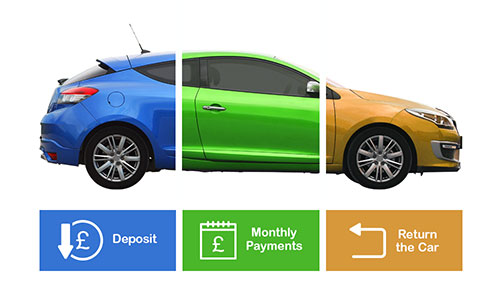

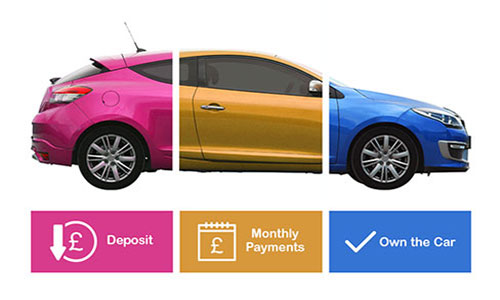

How does a Hire Purchase work?

Once you’ve found the car you want to buy, you will be able to apply for Hire Purchase finance. To do so, you will need to pass a credit check, which assesses your ability to meet the monthly repayments for the duration of your contract. Before signing on the dotted line, you must ensure the monthly repayments specified in your Hire Purchase agreement are affordable. Remember, failing to make your payments on time could result in your vehicle’s repossession and damage to your credit score. Most HP finance policies require the buyer to pay a deposit, which is usually around 10%. Some dealerships offer deposit contributions on new vehicles, but can sometimes recuperate these promotional costs elsewhere through a higher APR or an inflated list price. The car’s remaining value will be spread across a specified term, usually between 12 to 60 months.

Once you’ve made all of the repayments on your Hire Purchase agreement, you will have to pay an ‘Option to Purchase fee’ to transfer the ownership from the finance company. The amount will vary and will be specified in the contract. It’s essential you read the terms and conditions carefully before entering an agreement to ensure this figure is reasonable.

A Hire Purchase example

You are purchasing a car for £20,000 from a local dealership:

- A 10% deposit of £2,000 is required, leaving £18,000 owed on the car

- You opt for a 48-month agreement

- The dealership is offering a 5% APR deal, which will mean you have monthly payments of £414.53

- After four years (48 months) you will pay the ‘Option to purchase’ fee of £100

- In total, you would pay £21,997.44.

Benefits of a hire purchase

-

You own the car after you’ve made all the repayments, unlike a PCP where there is a large balloon payment if you want to own the car

-

The terms are flexible, usually between 12 and 60 months. However, the longer the finance term, the higher the overall cost due to interest payments

-

Fixed monthly repayments allow you to budget for other expenses month-to-month and manage your finances

-

You are more likely to be accepted for a Hire Purchase agreement than a personal loan due to the finance being secured against the car

-

There are no restrictions on mileage for the duration of the agreement

-

You won’t be charged for excess damage to the vehicle from the finance company at the end of the agreement

-

Manufacturers may provide deposit contributions, particularly on new vehicles.

Drawbacks of a hire purchase

-

If you fall behind on your monthly payments, the finance company could repossess the vehicle

-

A deposit of at least 10% of the car’s value is usually required

-

The car will be affected by depreciation; therefore, it may be worth considerably less at the end of the term

-

Monthly repayments are higher than PCP and PCH finance

-

You cannot modify or sell the car until you've made all of your payments

-

The car must be comprehensively insured for the full duration of the Hire Purchase agreement.

Ending a Hire Purchase agreement early

There is a clause in the Consumer Credit Act that allows you to end the contract early, known as ‘voluntary termination’. This clause allows drivers to terminate the agreement and return the car to the finance company provided they’ve made at least 50% of their repayments.

There are many reasons you may want to terminate your Hire Purchase agreement early. Financial changes, no longer requiring the car, or finding a cheaper alternative are all valid reasons. However, if you choose to terminate your HP agreement early, you’ll need to ensure the car is in good overall condition; otherwise, you’ll be liable for the costs of any necessary repairs.

If you want to terminate your HP agreement, but haven’t paid 50% of the contract’s amount, you will need to pay the difference before applying for voluntary termination. Remember to keep copies of any documentation, too, as this will prevent the finance company from claiming you defaulted on your payments, which would likely damage your credit score rating.